Key Takeaways

- Global low-carbon hydrogen production is set to rise to 0.84 mtpa in 2024, with a projected capacity of up to 65.3 mtpa by 2030.

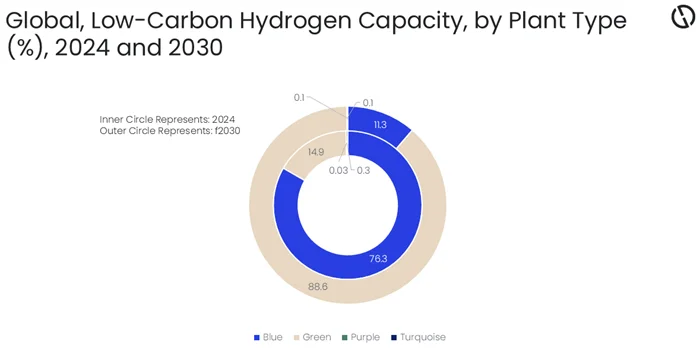

- Green hydrogen will dominate production with an 88.6% share by 2030, surpassing blue hydrogen’s share decline.

- The U.S., Canada, and Mexico are developing varied hydrogen policies, driving growth in the Americas region.

Overview of Low-Carbon Hydrogen Market Growth

Low-carbon hydrogen production has been relatively stagnant over the years but is poised for significant growth. Production is forecasted to increase to 0.84 million tons per annum (mtpa) in 2024, with total capacity reaching between 42 mtpa and 65.3 mtpa by 2030. The transition is primarily attributed to substantial capacity additions in the Americas, with green hydrogen expected to dominate at a projected 88.6% market share by 2030, overtaking blue hydrogen, which had a 76.3% share in 2024. These insights are derived from GlobalData’s report titled “Low-Carbon Hydrogen Market Report, Update 2025.”

As of 2024, the global production capacity for low-carbon hydrogen stands at 1.7 mtpa. Green hydrogen accounts for 14.9% of this total, while purple and turquoise hydrogen comprise 0.3% and 0.1%, respectively. By 2030, blue hydrogen’s market share is expected to fall to 11.3%, with purple and turquoise hydrogen remaining stable at 0.1% each.

The increase in hydrogen production is largely driven by various federal and state initiatives in the Americas, especially noteworthy in the U.S., Canada, and Mexico. According to Attaurrahman Ojindaram Saibasan, a Power Analyst at GlobalData, the hydrogen market in the Americas has seen robust growth due to these government actions, which vary in ambition and strategy across countries.

In the United States, momentum for hydrogen policy dates back to the early 2000s with the Energy Policy Act of 2005, which facilitated tax credits and loan guarantees for hydrogen production. Subsequent measures, like the American Recovery and Reinvestment Act of 2009, allocated funds for research and development. The Infrastructure Investment and Jobs Act (IIJA) signed in 2021 has further pushed hydrogen policy development by significantly increasing funding. Additionally, the Inflation Reduction Act (IRA) of 2022 introduced critical tax credits for clean hydrogen production.

The National Clean Hydrogen Strategy and Roadmap, released in 2022, outlines the U.S. strategy for achieving carbon neutrality, emphasizing the role of hydrogen in decarbonizing transportation and heavy industries. States such as California, New York, and Massachusetts are taking strong initiative at the state level. California, in particular, leads in promoting hydrogen fuel cell vehicles and developing supporting infrastructure.

Similarly, Canada’s Hydrogen Strategy, established in 2020, maps out the country’s vision of a robust hydrogen economy, focusing on clean production, infrastructure development, and export potential, especially to Europe and Asia. The Canadian government is backing these efforts with substantial financial commitments as outlined in Budget 2023. Provincial initiatives in British Columbia, Quebec, and Ontario are aligning with the national vision and harnessing regional advantages for hydrogen development.

Meanwhile, Mexico is still in the initial stages of exploring its hydrogen potential, focusing on utilizing local resources and its geographical advantages for production and export.

As the low-carbon hydrogen sector is expected to witness rapid expansion, it will still require significant scaling up of production capabilities to reduce costs and replace high-carbon hydrogen applications with more sustainable options, while also exploring new potential uses for hydrogen.

The content above is a summary. For more details, see the source article.